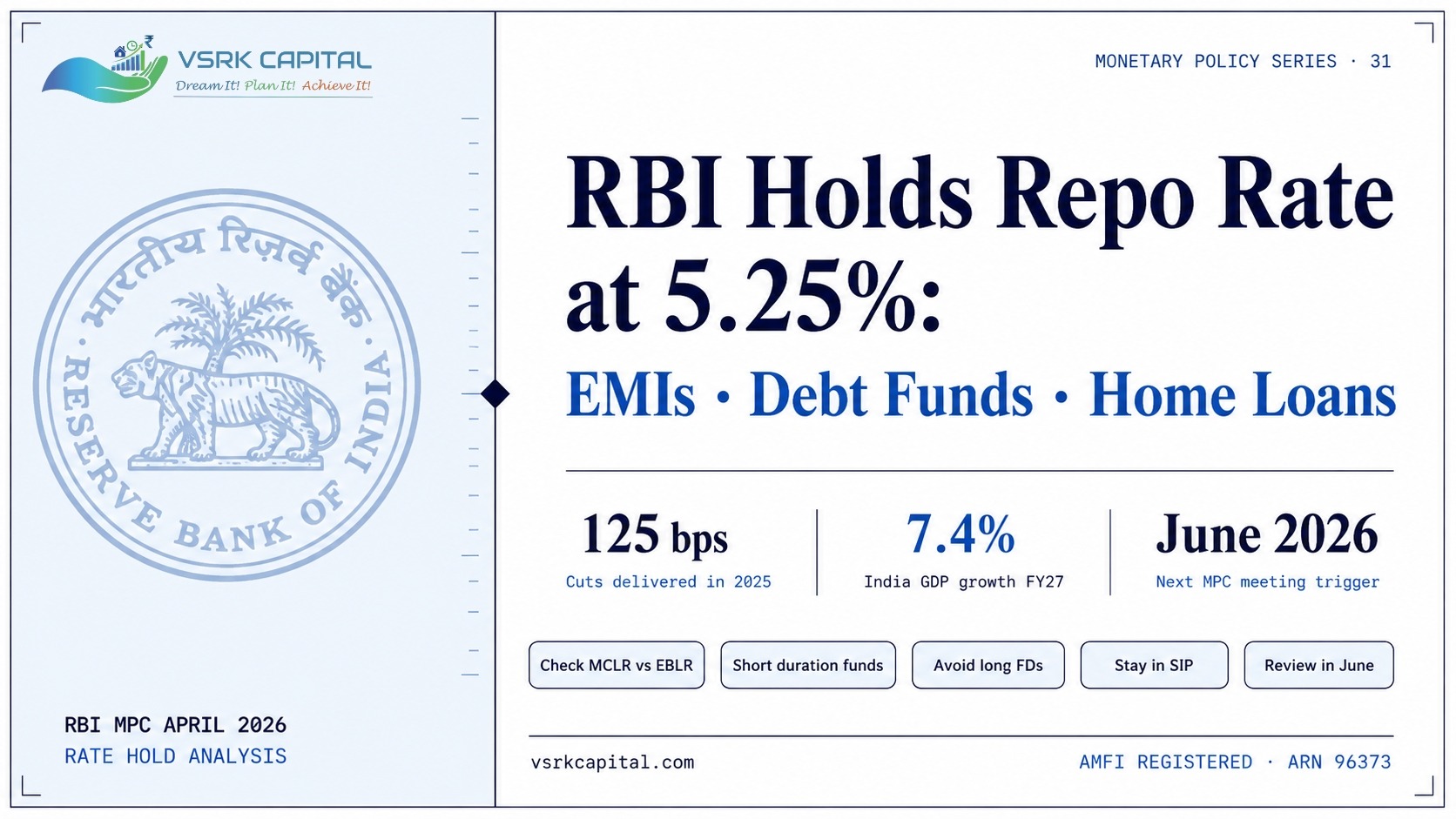

The Reserve Bank of India made its decision. The repo rate stays at 5.25%.

No cut. No hike. A pause.

For millions of Indian borrowers, home loan holders, FD investors, and mutual fund investors, this one number touches every corner of their financial life. And yet most people receive the news as a headline and move on without understanding what it actually means for their money in the months ahead.

Let us change that.

The Context You Need First

Before you react to this decision, understand where India’s rates stand today in historical terms.

The RBI cut rates aggressively throughout 2025, four times, delivering a cumulative 125 basis points of reduction, bringing the repo rate down from 6.50 percent to 5.25 percent. That is the most aggressive rate-cutting cycle India has seen since 2019. The pause in April 2026 and the continued hold at 5.25 percent are not a reversal of that trajectory. It is a deliberate pause to assess how inflation and global events, particularly the West Asia conflict and crude oil prices, develop before the next move.

The RBI projects inflation rising to approximately 4.2 percent by mid-2026, up from 3.2 percent in February 2026. GDP growth for FY2026-27 is projected at 7.4 percent. The central bank’s message is calm and clear: we have done our work, we are watching the data, and we will act when the conditions are right.

The next MPC meeting is scheduled for June 3 to 5, 2026. That meeting is likely to be more consequential than this one.

What It Means for Your Home Loan EMI

If you have a floating-rate home loan taken after October 2019, your loan is almost certainly linked to the External Benchmark Lending Rate, which moves directly with the repo rate.

The hold at 5.25 percent means your EMI does not change today. But here is the number that matters: borrowers who have been on EBLR-linked loans since before the 2025 rate cuts have already saved meaningfully. On a Rs. 50 lakh, 20-year loan, the 125 basis points of cuts delivered in 2025 translate to an EMI reduction of approximately Rs. 3,700 to Rs. 4,200 per month, depending on your bank’s spread. Those savings continue.

If you are still on an MCLR-linked loan from before 2019, you may not have received the full benefit of last year’s cuts. This is the moment to speak with your bank or a financial advisor about switching to an EBLR-linked structure.

What It Means for Your Debt Mutual Funds

This is where most investors need clear guidance.

When the rate-cutting cycle resumes, which is expected in the second half of 2026 if inflation remains controlled, long-duration debt funds will benefit significantly. Bond prices move inversely with interest rates. When rates fall, existing bonds with higher coupon rates become more valuable, pushing up the NAV of long-duration debt funds.

However, right now, with inflation rising toward 4.2 percent and global uncertainty from crude oil prices, a premature move into long-duration funds carries risk. If inflation forces the RBI to pause longer or even consider a hike in FY27, long-duration debt funds will underperform.

The more sensible positioning right now is short to medium-duration debt funds. They offer stability, decent returns above FD rates, and the flexibility to reposition when the rate direction becomes clearer after the June 2026 MPC meeting.

Liquid funds and money market funds remain the safest parking option for capital you may need within six to twelve months.

What It Means for Your Fixed Deposits

FD rates have already drifted lower through 2025 in line with the rate-cutting cycle. The hold at 5.25 percent means FD rates are unlikely to fall further in the immediate term. But they are also unlikely to rise.

If you are planning a long-term FD right now, exercise caution. If inflation persists and the RBI delays further cuts or considers a hike in FY27, rates could eventually move upward. Locking in a five-year FD at current rates could mean missing a better rate later in the year.

The practical guidance: keep FD tenures shorter, six months to one year, until June’s MPC meeting gives a clearer signal.

5 Calm Steps for the Current Environment

- Do not restructure your entire portfolio on a rate hold. This is a pause, not a pivot. Stay calibrated.

- Check if your home loan is still on MCLR. If yes, calculate the savings from switching to EBLR. Your bank is obligated to facilitate this.

- Move into short to medium-duration debt funds. Avoid the temptation of long-duration funds until the June MPC meeting provides clearer direction.

- Avoid locking long-tenure FDs. Keep tenures under twelve months until the rate direction is confirmed.

- Stay invested in equity SIPs. Rate policy does not change the long-term equity story. India’s GDP growth at 7.4 percent is still the most compelling case in emerging markets.

The Bottom Line

A rate hold is not bad news. It is a signal of stability and caution. The RBI sees the same global volatility you do. It is choosing deliberate patience over reactive policy, and that is the right call for an economy growing at 7.4 percent with rising but manageable inflation.

At VSRK Capital, we help you read these signals and translate them into the right portfolio decisions, not the loudest ones.

Speak with us before the June 2026 MPC meeting. Because that decision may require you to move quickly.

Disclaimer: This content is for educational and informational purposes only. It does not constitute financial, legal, or investment advice. Investments are subject to market risks. Please read all scheme-related documents carefully before investing. VSRK Capital is an AMFI Registered Mutual Fund Distributor. ARN 96373.