AMFI- Registered Mutual Fund Distributor - VSRK Capital

📈 Investing doesn’t have to be complicated. Join VSRK Capital to explore SIPs, mutual funds, and disciplined wealth-building. Backed by 18+ years of trust. Talk to us today and start your journey.

In these abysmal times of ongoing pandemic and unstable market dynamics, the markets have been highly affected due to the investor consternation and fall in demand. It is said that around 59 lakh SIPs have been stopped, however, it has been observed that at the time when many SIPs have been either stopped or paused there has been additional inflow made by some investors cushioning the SIPs inflow. We would like to suggest some reasons you should consider before deciding whether you should continue your investment in SIPs or not.

Lower Valuation One of the prime causes leading to the discontinuation of SIPs is the fall in the values of your investment. Before going more into this let’s briefly talk about the nature of the bearish phase that the country is going through at the moment. The important characteristic of the bearish phase is that it is temporary and after the end of such phase there is always a bullish market where the overall market is highly satisfying. This means that currently, the stocks are available at lower prices than what they were at a month ago. Such circumstances could be seen as a chance to invest in more units at lower costs.

Constant Benefits from Power of Compounding Known as the 8th wonder of the world, Compounding is one of the major reasons to continue investing irrespective of the market volatility. By making regular investments and reinvestment of the returns generated on such investment, the power of compounding helps the investors in making contented returns.

Essence of long-term growth The markets have always been volatile and subject to uneven fluctuations, however, one thing that has always been static in this environment is the immense potential for wealth creation. It is said that in the past 40 years irrespective of multiple recessions and downfall of the economy at various situations the investors have gained an overall 16% compounded annual returns in S&P BSE Sensex since its inception.

Lack of Re-Investment Alternatives If one decides to withdraw the funds there should be an alternative for the use for such finds otherwise the main objective of investing it in the first place won’t be accomplished. If the sole reason was the factor of fall in markets it is advisable to consult your professional fund manager before making any rash decisions.

Opportunity to earn more As discussed earlier the bearish phases do not sustain for long, which allows you to buy some good stocks at currently low market prices but apart from this there is an additional chance of averaging out the total cost of portfolio. It is highly possible that due to high market prices you might have overpaid for your holdings and now could be a good time to make up for the additional costs incurred.

Mutual fund is an investment fund where multiple investors pool their money to purchase securities. Such funds are managed by a highly trained professional commonly known as a fund manager or portfolio manager. Due to factors like benefit of diversification and comparatively stable returns, mutual funds have become one of the most looked after investment options.

When you opt for mutual funds you can invest through 2 schemes i.e. through regular or direct schemes. Let’s briefly talk about both the schemes. Direct investment plan is where an investor can directly invest into the company’s plans, generally through its website. Regular investment plan is where you buy the same securities through an advisor.

What is the Difference Between Regular and Direct Schemes?

In direct schemes the expense ratio is low as no brokerage is paid to any adviser resulting in comparatively high returns as compared to the indirect schemes. However, the major problem with these schemes is the lack of professional advice. Here, it is very common for people to make wrong decision and lose all the hard-earned money.

The investor, himself, has to do market research and analysis. In making any investment decision there are a lot factors to be kept in mind such as the market outlook, investment objective, rate of inflation, periodical readjustment of portfolio, etc. These require a lot of time & labor and require special knowledge of the financial markets which a common investor may not possess.

In indirect schemes, a brokerage is paid to the adviser. So, the expense ratio is high making the returns lower than returns on direct plan. But, it shall be noted that such brokerage is generally very less compared to the reduction in risk which is the main goal of any financial advisor.

However, the main merit of such indirect scheme is the presence of a professional adviser. Any investment decision made by the investor is guided by the professional supervision of a financial planner hired by the investor.

Such financial planner is usually a person who has high expertise in financial analysis and planning. He uses his knowledge into finding the best alternative for meeting the client’s requirement and fulfilling the ultimate financial objective. Therefore, here the risk of losing investment or non-achievement of investment objective is low as compared to direct schemes.

Which Plan is Better For You?

Each plan has its own merits and demerits. It is clear that direct plan has more benefits to it. However, the associated risk of uninformed investment is also very high. One wrong decision could lead to loss of all your money. Hence, it could be concluded that only those with good knowledge of financial markets shall primarily use direct plans. A person with lack of such knowledge and expertise is advised to invest in indirect schemes and use the help of a professional adviser.

All the successful investors suggest one thing in common i.e. having more than 3 sources of income. Having such extra sources apart from salary and profits from business help you in times of uncertainty such as the current covid-19 situations where millions of people have lost their jobs and businesses faced huge losses. So, here we will talk about various sources of passive income.

What is Passive Income?

Firstly, let’s talk about the concept of passive income. Passive income is an additional source of income. Such sources are generally side-hustles and use the innate talent of an individual. Such side-businesses are built around personal hobbies of an individual such as writing, painting, dancing, photography and videography. Generation of income from such sources is initially very difficult and requires a lot of passion and hard work. In the starting, the cash receipts from such adventures are often very low but in the long run they are seen to provide even better cash flows than the primary income. Apart from the extra income generation there are many other benefits such as freedom, flexibility and recurring income.

Top 8 Sources to Earn Passive Income

Blogging

This is one of the most popular sources of extra income and is often taken by the individuals who have an interest in creative writing. Here, you have the freedom for writing on any topic ranging from a blog on fitness to blog about music instruments. This requires a good knowledge about the topic you are writing on and a keen desire to share your knowledge with the world. Running advertising and engaging in affiliate marketing are great ways to generate income from your blogs. You can use sites such as Blogger and WordPress for writing blogs.

YouTube Channel

Generating income from creating and uploading videos on YouTube is one of the most popular ways to earn passive income. Here, you just need to create a YouTube channel and upload videos. Once your channel becomes popular you can start earning by applying for an advertising program offered by YouTube.

Consultancy Business

This source includes a large variety of professional services that you may provide to your clients. You can serve as an investment consultant, property consultant, tax consultant or business consultant. Here you require good knowledge and expertise in your area of expertise.

Freelancing

Freelancing is a highly preferred method for generating passive income. Here you just need to use your skills for completing a project assigned to you by your clients. This requires having a skill such as digital marketing, writing, web designing, income tax return filing, etc. Websites such as Fiverr, Upwork provides you a platform to start freelancing and earn a good passive income.

Affiliate Marketing

If you have searched about how to make money online you must have read about affiliate marketing. Here you need to recommend products to people and if they buy the product from the link shared by you, you will receive commission. Famous websites such as Amazon and Flipkart provide a facility for becoming an affiliate marketer.

Teaching Online Course

In this Covid19 struck environment, the demand for online tutoring has increased. Here, you need to have the knowledge about a subject matter or a skill and design an online course. Websites such as Udemy or Thinkific provide a facility for an online course.

Investment in Mutual Funds & Equity for Dividend

The simplest idea to generate passive income is through investment in mutual funds and equity. Such investments generate income in firm of dividends.

Insurance Agency

Another source of generating passive income is through working as a part-time insurance agent. Here you will have to sell insurance policies and you will be paid commission on the premium paid by the customer. You can sell various types of insurance such as medical insurance, life insurance, general insurance etc.

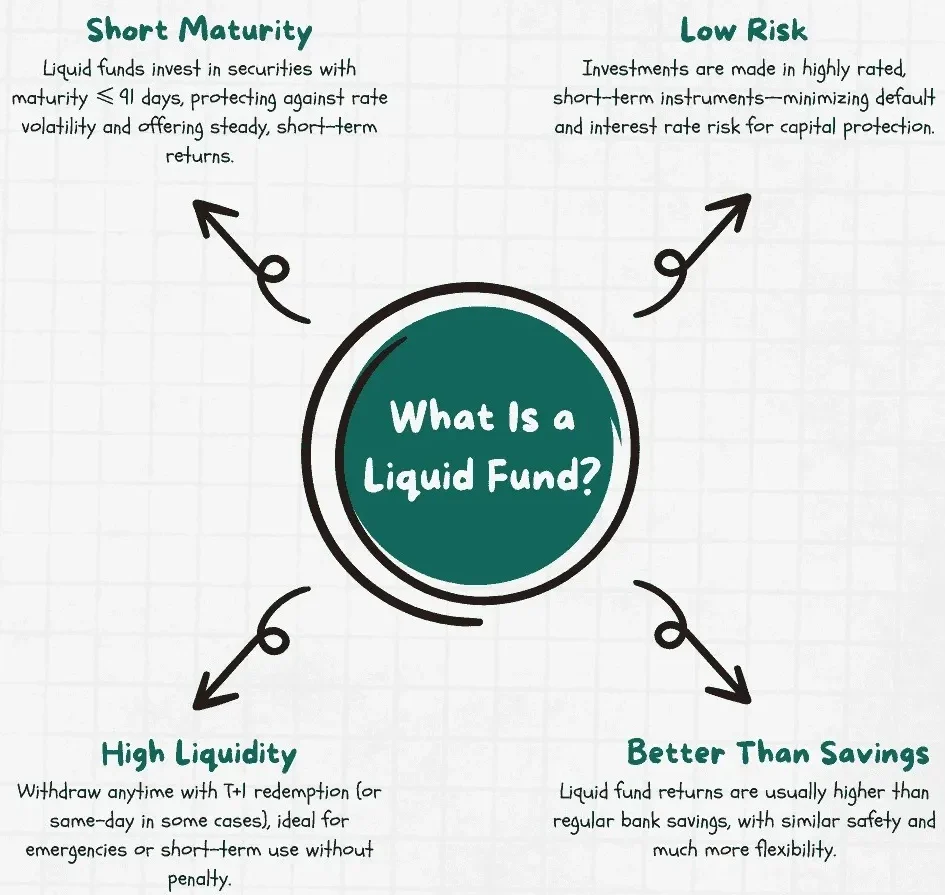

Money invested in liquid funds can be said to have great liquidity with very small risk and interest return over a savings bank facility, as liquid funds are debt mutual funds that invest in short-term instruments like Treasury Bills, commercial papers, and certificates of deposits. Let us discuss those characteristics, investment benefits in liquid funds, and how liquid mutual funds can rightly fit your requirements.

What Is a Liquid Fund, Anyway?

Short maturity:

Liquid funds invest their money in debt securities with maturities of 91 days or less, protecting themselves from interest rate movements and generating stable returns with less volatility, making them ideal for short-term requirements.

Low risk:

As liquid funds are invested in high-rated, short-term securities, they are exposed to low default and interest rate risk. They thus can be considered a low-risk investment for cautious investors requiring capital preservation and stability.

High liquidity:

Investors can redeem their investment in liquid funds quickly, often receiving the funds within 24 hours, making them ideal for emergency needs or short-term cash management without penalties.

Advantages of Liquid Fund Investments

Better Returns Than Savings Accounts

Liquid fund returns typically exceed bank savings rates, giving you more yield on idle money.

Same-Day Liquidity

You can withdraw the amount instantaneously, with no lock-ins, so liquid mutual funds are ideal for unforeseen expenses.

Low Volatility

Invested carefully, a liquid fund sees little price volatility, ensuring your capital is secure.

Tax Efficiency

Short-term capital gains are taxed, but still better off compared to FD interest.

Ideal For Cash Management

Waiting for a lump-sum investment, liquid funds fill the gap safely and effectively.

How Liquid Funds Work

Asset mix:

These instruments, such as government securities, certificates of deposit (CDs), and commercial papers (CPs), are maintained in liquid funds to secure investors, liquidity, and interest risk.

Role of fund manager:

The fund manager achieves portfolio stability by choosing high-grade, short-term securities, balancing safety and return cautiously, and matching with investor liquidity requirements and regulatory requirements.

Fluctuation in NAV

As liquid funds contain securities with extremely short tenors, their Net Asset Value (NAV) fluctuates minimally, providing stable returns and hence suitable for low-risk, short-term investments.

Who Should Invest in Liquid Mutual Funds?

Emergency corpus builders:

Liquid mutual funds are best suited for creating an emergency corpus owing to fast redemption, typically within 24 hours, allowing instant access to funds during medical, financial, or personal emergencies.

Lump-sum investors:

Large-scale investors can keep their money invested in liquid funds temporarily to gain returns as they look for long-term investments or wait for better market conditions.

Salary accounts:

Professionals can utilize liquid funds to set aside excess salary balances, providing a buffer for monthly spending while enjoying higher returns than savings bank accounts.

Conservative investors:

Those who shun market risk and desire low-risk capital preservation can opt for liquid funds for steady, small returns without exposure to the direct stock market.

Benefits of Liquid Fund — In-Depth

1. Stability and Security

Liquid funds invest in high-credit-rating products only. The low duration shields against interest-rate shocks.

2. Ease of Access

Liquid funds can be redeemed almost immediately, in contrast to FDs with charges. Liquid mutual funds provide same-day or T+1 redemption.

3. Tax Transparency

Liquid funds demonstrate transparent capital gains taxes. Contrast liquid fund gains with savings account income for transparency.

4. Flexibility

Liquid funds are Perfect for cash cushions. Shift funds seamlessly into long-term schemes.

5. Expert Management

Fund managers manage liquid funds actively for maximum risk-adjusted returns. Investors get the advantage of professional portfolio management.

Comparison of Liquid Funds vs Other Instruments

Feature

Liquid Funds

Savings Account / Fixed Deposit (FD)

Liquidity

Redemption in T+0 or T+1

Partial withdrawal with penalty (FD); Anytime for Savings

Returns (FY 2024)

4–6% p.a. (historical data)

3–5% (Savings) / 6–7% (FDs)

Volatility

Low

None

Taxation

Treated as a debt fund – taxed based on holding period

Taxable as per the income slab

Use Cases

Parking idle cash, emergency corpus

Daily expenses (Savings) / Short-term goals (FD)

Risks and Considerations

Credit risk: A small default would affect the returns.

Interest rate changes: Higher rates will decrease NAV slightly.

Tax implications: Gains within 3 years are taxed according to income slabs.

Expense ratio: Even low-cost liquid mutual funds have charges that impact returns.

When to Use Liquid Funds

Creating an emergency fund.

Parking funds before a large investment.

Managing salary or dividend receipts.

Keeping funds for the short term during market dips.

How VSRK Capital Can Help

At VSRK Capital, we facilitate prudent aging of cash via liquid funds:

Expert Guidance: Select proper liquid mutual funds according to your cash flow requirements.

Portfolio Construction: Portfolio with long-term funds to save tax and growth.

Real-Time Rebalancing: Track and rebalance your liquid fund exposure concerning changing goals.

A debt fund with investment in highly liquid financial instruments for short-term financial requirements.

What are the benefits of a liquid fund?

Pockets higher returns than bank deposits, low risk, same-day liquidity, and expert management.

Are liquid mutual funds secure?

Generally secure, but not riskless—credit and interest rate changes can impact returns to a minimal extent.

Can I keep emergency funds in a liquid fund?

Yes, due to their high withdrawal facility, they are best suited for emergencies.

How are liquid funds different from overnight funds?

Liquid funds have up to 91 days of maturity, while overnight funds work on one-day instruments alone.

Conclusion

Liquid funds provide an astute, versatile means of handling short-term cash at a better-than-savings interest, and so are an indispensable component of any portfolio. With the benefits of liquid fund investment, such as stability, liquidity, and transparency, these instruments fill the gap between cash and structured investments.

VSRK Capital helps you choose the most suitable liquid mutual funds for your requirement—either creating a corpus for emergency needs or holding out for a better opportunity. Go to VSRK Capital and discover more, and begin wisely managing your short-term money.

What’s Next

Determine your cash-buffer requirement and time frame.

Compare fund performance and returns data.

Automate investments into a liquid fund for regularity.

In the past few weeks, the stock prices have fallen drastically and the market saw a downfall of nearly a third of the global market cap. The whole world has been badly affected by the spread of the virus forcing companies to shut down, heavy unemployment and huge downfall in the economy. Almost all major most economic activities have impacted by the disease. The markets have been heavily damaged by the Covid 19 and the effects are visible on the global economic growth. The global gross domestic product (GDP) growth projection for 2020 has halved by the Organization for Economic Co-operation and Development (OECD).

Current Situation in Indian Markets

Although, the market has slightly started to rise slowly such sudden fall in stock valuations and other instabilities have triggered panic across the world and shaken the confidence of investors. The past Friday turned out to be in favour of the investors. In the end, Sensex stood at closed 20% below the peak achieved two months ago whilst other markets which have fallen more.

When the equity and debt instruments were already hit badly, the crude oil war between Saudi Arabia and Russia has only worsened the economic conditions injecting volatility into other assets. Now, the economic tension has extended to currency and commodities market.

Suggested Measures for Ensuring Financial Safety of Investments

Investment professional prefers investment in high performing- financially strong stocks with relatively higher earnings & profitability, solid balance sheets, bigger cash flows, and more effective management should be preferred. At the same time, professional advisers also suggest equity investors alter their portfolio allocation towards large-cap and multi-cap stocks as the market correction might be a little prevalent in the short term.

It might be suggested this is a good time for long term investors to buy high valuation stocks at low levels. For making a profitable investment and subsequent appreciation in the investments value few conditions shall be seen such as high-profit margin stock, low debt and innate capability & financial soundness to sustain even if the share prices touch the rock bottom due to instabilities.

The more-safe investment options might also be suggestible like Corporate Bond funds / Banking & PSU Debt Fund which provide more reliability and trustworthiness in future which seems highly dynamic due to the highly volatile markets.

Stock exchanges are markets where the participants come together for buying and selling of financial instruments such as shares, debentures, bonds, etc. it is run by set rules and regulations set by appropriate bodies such as SEBI in India. Only the securities of listed companies are traded with stock exchanges. All such stock exchanges shall be recognized by the government and only registered brokers and members are allowed to trade instruments on it.

There are around 9 official Stock Exchanges in India-

Bombay Stock Exchange (BSE)

National Stock Exchange of India (NSE)

Calcutta Stock Exchange

India International Exchange (India INX)

Indian Commodity Exchange (ICEX)

Metropolitan Stock Exchange of India Ltd. (MSE)

Multi Commodity Exchange of India Ltd. (MCX)

National Commodity & Derivatives Exchange Ltd. (NCDEX)

A mutual fund is one of the most popular modes of investment opt by investors desirous of making good returns on the same. There are generally only 2 ways to invest in a mutual funds scheme- Lump sum investment and Systematic Investment Plan.

Lump-sum investment refers to the investment of a good sum of money once into the scheme. It is suitable for times when you have a free load of cash in hand with you. However, the availability of a comparatively huge sum of money is not very common and this is the reason why many potential investors were unable to make investments.

Systematic Investment Plan (SIP) was brought as a mean of making a systematic and regular investment. This requires the investors to invest a fixed amount of funds at stated intervals, regularly. This has dealt with the inability of huge sums and allows the common man a chance to invest.

The return from the mutual funds depends on the market value of the securities present in the portfolio represented by the Net Asset Value (NAV) of the mutual fund scheme. Hence, the NAV keeps fluctuating on a daily basis, which is more prominent under equity mutual funds.

Mutual funds are one of the most popular financial instruments in town. Mutual fund is a collection of funds pooled in by investors and managed by a portfolio manager. Such funds are invested into various schemes in accordance to the earlier set objectives.

While the above information is generally available on all the online sites, the actual working of such funds isn’t told with much clarity and we ought to clear all your doubts on the actual working of mutual funds. So, let’s start.

As mentioned earlier mutual funds are a pool of resources instead of being a single resource which means there are multiple investors who have put money in a fund. Each person who has invested their money into the fund gain ownership over a part of the fund, known as a unit. We can also say that the entire fund is subdivided into multiple parts known as units. So, when a person wants to invest in a fund he has to buy these units.

Such mutual funds are of many types like equity funds, debt funds, hybrid funds, income funds, growth funds, index funds etc. Each fund has its own objectives, risk & reward. Different investment bankers offer different schemes. You may select the one which favors your objectives the most.

When you select the scheme you want to invest into, you have to buy the units. Once you buy the units, the investment bankers allocate the money to that fund. Generally, under the umbrella of a mutual fund there are many companies under it. They are known as sub-holdings.

Let’s understand this more clearly with an example of an equity mutual fund. Normally such mutual funds allocate around 70% of the total corpus in equity, 18% in debt and 12% in other securities. Within such umbrella of securities, there are a large number of companies.

The investment of money into a various types of securities a dividend supported by fixed returns. Also, within such types of securities, example- equity, there are a lot of companies existing in various sectors such as banking, refineries, housing finance and construction, etc. This helps the corpus through the benefit of diversification so that if any of these sectors under performs there is a low impact on the overall value of investment.

Mutual fund is an investment fund where multiple investors pool their money to purchase securities. Such funds are managed by a highly trained professional commonly known as a fund manager or portfolio manager. This individual invests this corpus of funds into different securities such as stocks, debentures, bonds, gold, etc. as per the objective of the fund and with the aim of reaping profits out of such investment.

Let’s understand this more clearly with an example of a mutual fund known as Hybrid Equity Fund. Normally, all invest such mutual funds around 70% of the total corpus in equity, 18% in debt and 12% in other securities. Within such umbrella of securities, there are a large number of companies.

The investment of money into a various types of securities a dividend supported by fixed returns. Also, within such types of securities, example- equity, there are a lot of companies existing in various sectors such as banking, refineries, housing finance and construction, etc. This helps the corpus through the benefit of diversification so that if any of these sectors under performs there is a low impact on the overall value of investment.

Investing refers to the process of setting out a certain sum of money for a set purpose and participating in certain securities which help in the achievement of the objective for which such investments are created. The sole purpose of such investment is to earn profits in the course of investment in such funds & securities.

Diversify your assets & associated risks

Economic assets are of essential value to our livelihood especially in times of extreme difficulties such as the ongoing pandemic. Distributing your money into several modes of investment and investing in various securities helps us to minimize the associated risks.

Saving money loses to inflation

After making the necessary expenses a lot of us set aside the amount left. However, due to the effects of inflation and the concept of time value of money such amounts kept in our wallets or savings bank accounts continuously lose their actual value.

For example- If the rate of inflation is 2% per annum and you could buy 1 kg apple for INR 100 toda, the next year it would cost INR 102 for the same 1 kg of apples and similarly after 10 years the same 1 kg apple would cost you around INR 120.

Due to the inherent limitation of time value, saving is not the best option. Investing such saved funds helps you fight the effects of inflation by generating returns in the form of dividend or interests or in such other manner as maybe applicable.

Increases earning potential

Making informed investment helps you in many ways such as reducing the risks of losing all the money by diversification as well as generating revenues in the form of interest, dividend, etc. Such extra income helps in increasing the earning potential in many ways. You may use the extra amount in starting a new venture, initiating a side hustle or just further investing such an amount.

Power of compounding

Compounding is said to be the 8th wonder of the world. The power of compounding could be understood by the following example- if you start investing INR 500 month for the next 40 years at 18% interest rate per annum the total investment over the period would be just INR 2.4 Lac but the accumulated value received would be INR 4.29 Crores.

Get tax benefits

The Income Tax Act provides various exemptions and deductions from the taxable income. So, for example- if you were falling under the 30% tax slab and you make an eligible investment of INR 1 Lac you save around INR 30,000 just by making such an investment as you won’t have to pay the tax on the same.