May 19, 2026

You opened your mutual fund app this week, and the numbers...

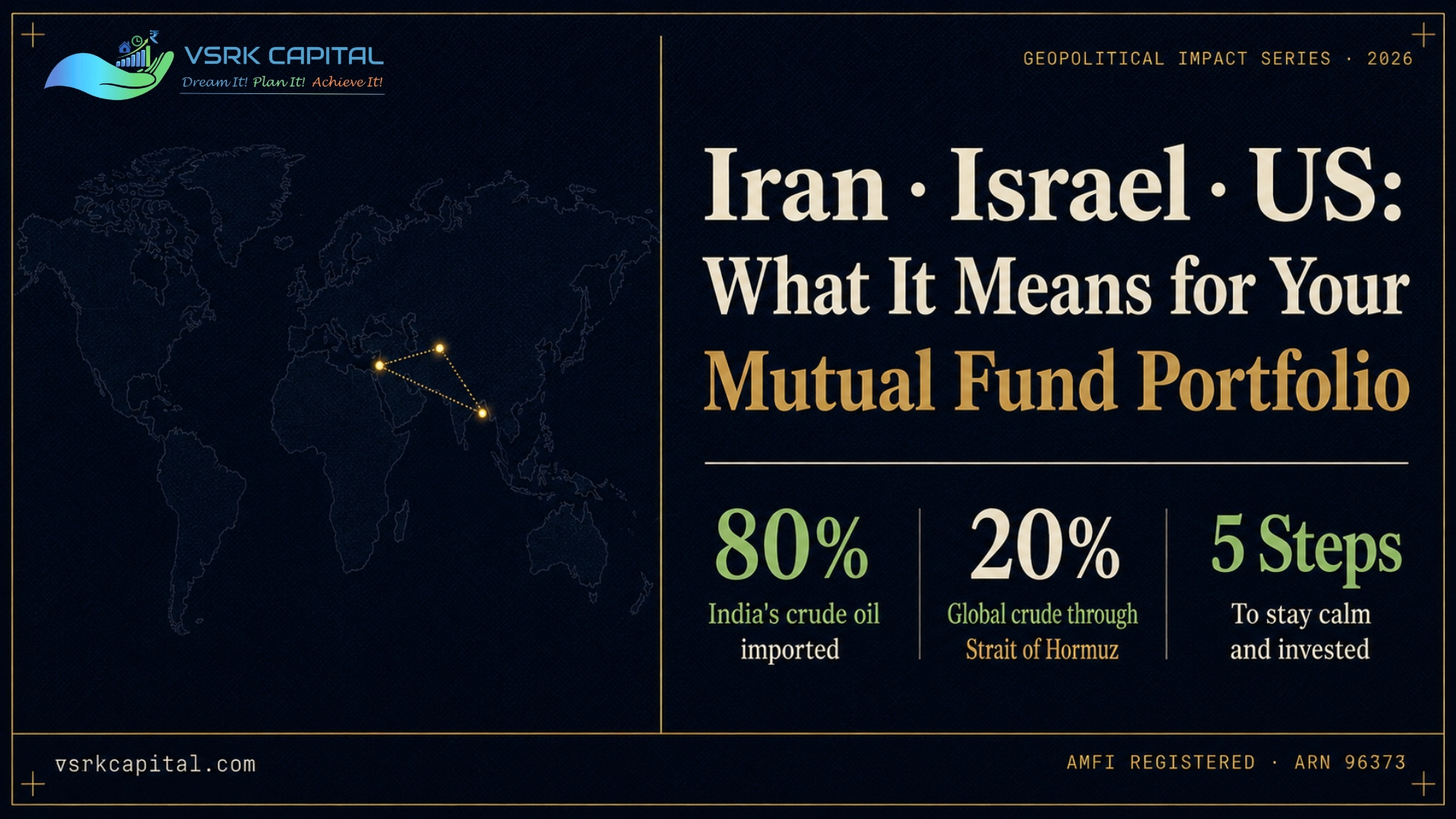

You opened your mutual fund app this week, and the numbers...

Somewhere between a Monday morning commute and a late-night deadline, a...

In a world where fixed deposits offer 7 percent and equity...

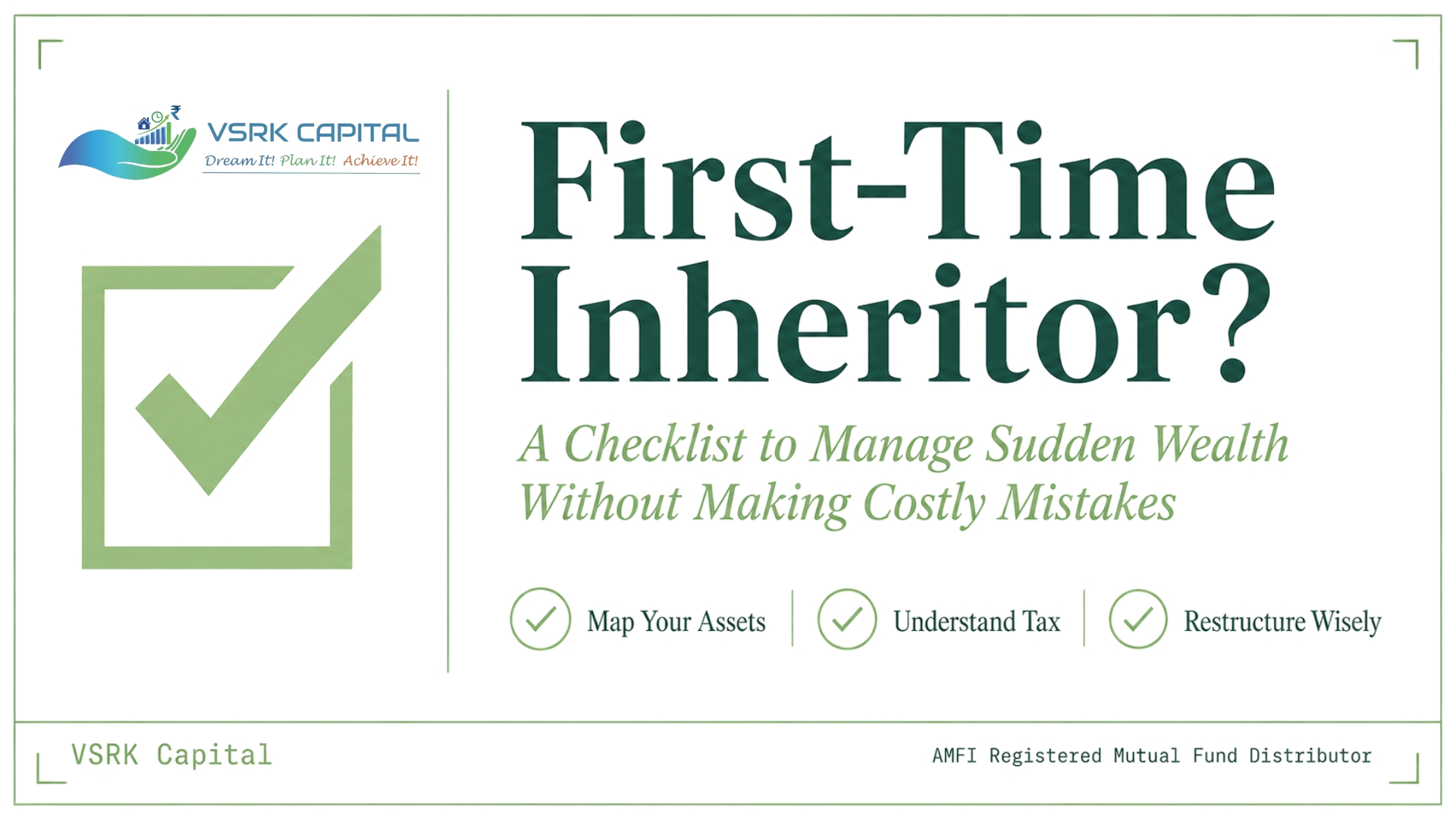

Nobody prepares you for the moment you become wealthy overnight. One...

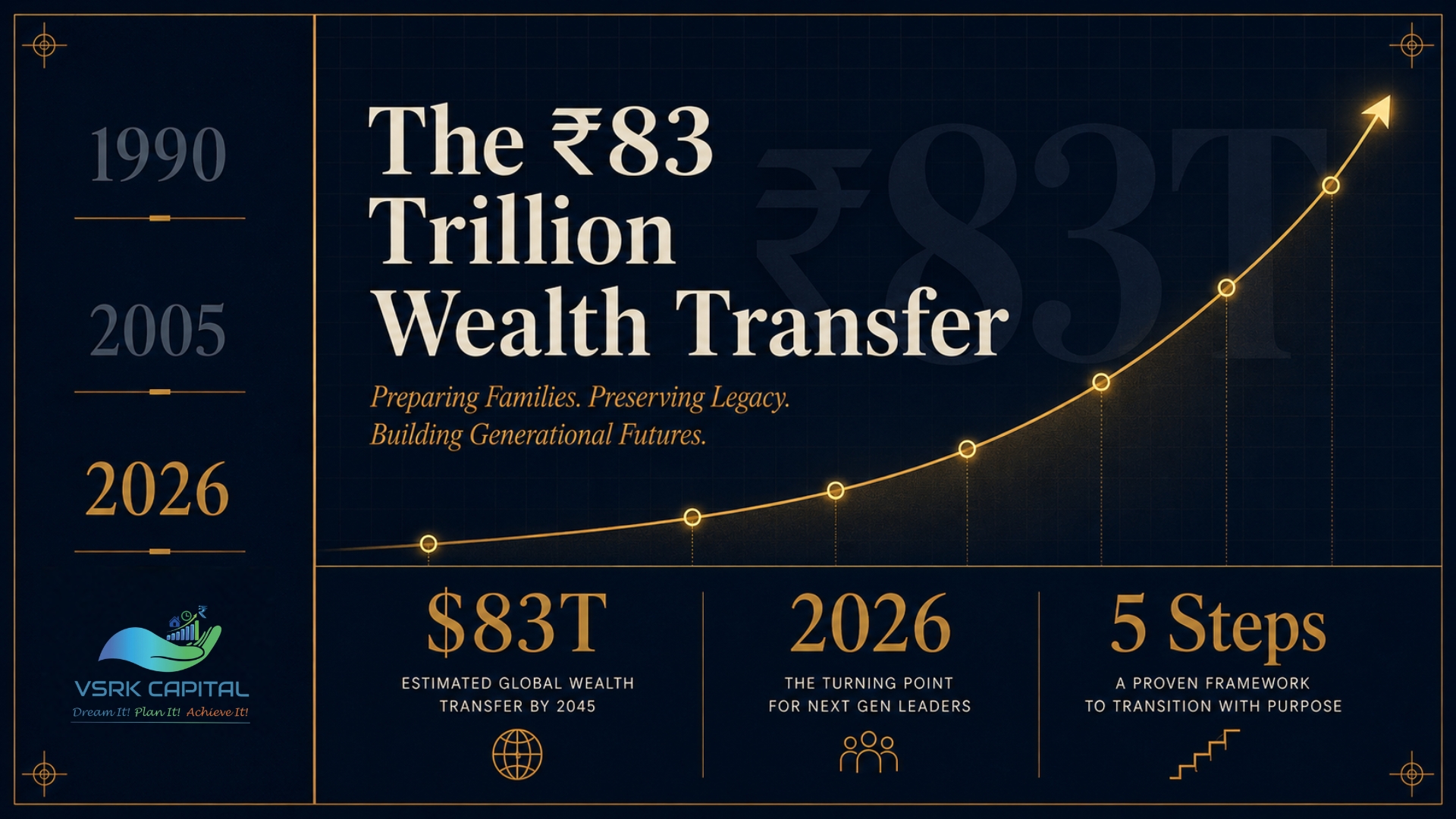

A quiet financial revolution is unfolding across Indian households right now,...

How Can I Buy Index Funds Without A Demat Account? Table...

Systematic Investment Plans (SIPs) have become one of the most popular...

Artificial intelligence has stopped being a buzzword in finance. It’s now...

Nurturing Growth with Structure and Care Maa Skandamata symbolizes nurturing, guidance,...